Understanding the Updated FASB Guidance for Crypto Asset Accounting

On September 6th, 2023, a landmark update was introduced by the Financial Accounting Standards Board (FASB) targeting the accounting practices for crypto assets.

This significant revision, which became effective on December 14th, 2023, mandates the transition from the traditional cost-based accounting method to the fair value approach for qualifying crypto assets. The intent behind this change is to foster greater transparency and standardization within the rapidly evolving digital asset sector.

In this article, we’re diving into the specifics of the FASB's new guidelines and how Bitwave's solution effectively addresses these changes in the crypto accounting landscape.

Why ASU 2023-08 is a Big Deal

ASU 2023-08 allows entities that hold crypto assets on their books to recognize them at fair value rather than the previous accounting method of treating them as indefinite-lived intangible assets subject to impairment.

Why the New Guidance

The Update document highlights the reason for the change, saying that the previous accounting method didn’t provide investors, lenders, and creditors with decision-useful information, specifically:

“Accounting for only the decreases, but not the increases, in the value of crypto assets in the financial statements until they are sold does not provide relevant information that reflects (1) the underlying economics of those assets and (2) an entity’s financial position.”

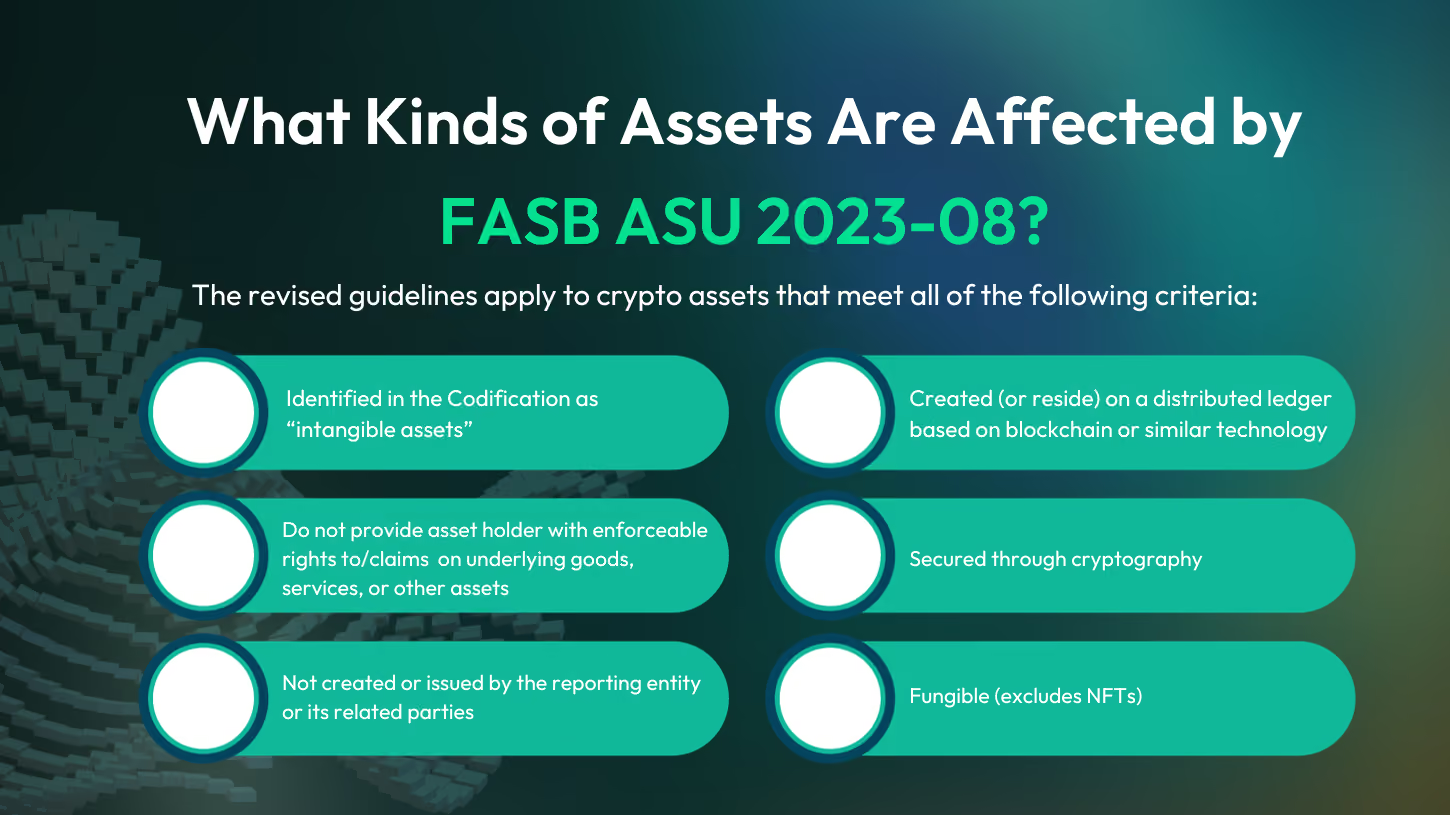

What Kinds of Assets Are Affected

The revised guidelines apply to crypto assets that meet all of the following criteria:

- Identified in the Codification as “intangible assets”

- Do not provide the asset holder with enforceable rights to or claims on underlying goods, services, or other assets

- Are created or reside on a distributed ledger based on blockchain or similar technology

- Are secured through cryptography

- Are fungible

- Are not created or issued by the reporting entity or its related parties

It’s worth noting that the updated guidance doesn’t encompass all types of digital assets. Specifically, nonfungible tokens (NFTs) and wrapped tokens fall outside this scope.

For NFTs, financial statement preparers must thoroughly understand the rights and transfers associated with these tokens. Wrapped tokens are also excluded as they often represent a right or claim to another asset, and their varied nature could lead to unintended implications under the new guidance.

Therefore, entities may need to adhere to the traditional intangible asset model or other accounting methods for these tokens.

Transitioning To The New Standard

Effective Date

The new regulations offer an option for early adoption after December 14th, 2023. Adoption is mandatory for all entities starting December 15th, 2024, including the interim periods within those fiscal years.

8 Steps to Making a Smooth Transition

To transition to FASB ASU 2023-08, an entity would need to follow these steps:

1. Determine the Scope of Applicable Crypto Assets: Ensure the crypto assets fall under the defined criteria in the ASU, such as being fungible, residing on a blockchain, and not being issued by the entity itself.

2. Assess Current Accounting Practices: Review how crypto assets are currently accounted for in the financial statements. This involves understanding the existing carrying amount of these assets.

3. Calculate the Fair Value of Crypto Assets: At the beginning of the annual reporting period when the entity first applies the ASU, determine the fair value of each applicable crypto asset.

4. Journal Entry for Adjusting Retained Earnings: Record a journal entry to adjust the opening balance of retained earnings or other equity components according to Subtopic 350-60-65-1:

“b. An entity shall recognize the cumulative effect of initially applying the pending content that links to this paragraph as an adjustment to the opening balance of retained earnings (or other appropriate components of equity or net assets in the statement of financial position) as of the beginning of the annual reporting period in which the entity first applies the pending content that links to this paragraph.

c. The adjustment to the opening balance of retained earnings (or other appropriate components of equity or net assets in the statement of financial position) shall be calculated as the difference between the carrying amount of crypto assets as of the end of the prior annual reporting period and the fair value of those crypto assets as of the beginning of the annual reporting period in which the entity first applies the pending content that links to this paragraph.”

5. Documentation and Disclosure: Prepare adequate documentation and disclosures as required by the ASU, detailing the nature of the crypto assets, the basis for fair value measurement, and the impact of the transition on the financial statements.

6. Ongoing Fair Value Measurement: Implement processes for ongoing fair value measurement of crypto assets, as subsequent changes in fair value are to be recognized in net income each reporting period.

7. Training and System Upgrades: Train staff and upgrade accounting systems as necessary to ensure ongoing compliance with the new standard, including fair value measurement and reporting.

8. External Review and Audit Considerations: Engage with external auditors or advisors to review the transition process and ensure compliance with the new standard.

ASU 2023-08 Disclosure Requirements

The revised standards mandate detailed disclosures for both annual and interim periods, empowering investors with essential insights for evaluating the risks and exposure related to significant crypto asset holdings.

Here’s a summary of the disclosure requirements (for full requirements, refer to ASU 350-60-50):

Interim and Annual Reporting

Disclose for each significant crypto asset:

- Name, cost basis, fair value, and number of units held.

- Aggregated cost bases and fair values of non-significant holdings.

Annual Reporting

- Disclose the method used for computing gains/losses (e.g., FIFO, specific identification, average cost).

- If not separate, disclose the income statement line item where gains/losses are reported.

Annual Reconciliation

- Provide an aggregate reconciliation from opening to closing balances.

- Separately disclose changes due to additions, dispositions, gains, and losses.

- Describe activities leading to additions (e.g., purchases, receipts from customers, or mining activities) and dispositions (e.g., sales or use as payment for services)

- Disclose total cumulative realized gains/losses from dispositions.

Contractual Sale Restrictions

- Disclose fair value, nature, and duration of restrictions.

- Circumstances causing restriction lapses.

- Determine necessary detail level, emphasis, aggregation/disaggregation.

- Assess if additional information is needed for financial statement users.

Exceptions for Immediate Conversion

- Entities converting received crypto assets into cash nearly immediately are exempt from certain disclosures.

Streamlining Fair Value Accounting with Bitwave

As finance and accounting professionals grapple with the complexities of the new FASB fair value accounting standards for crypto assets, it's crucial to have tools that not only simplify compliance but also enhance financial reporting accuracy.

Bitwave is your dedicated partner to ensure a smooth transition, offering an array of features tailored to meet the nuanced demands of the digital asset sector.

Custom Inventory Groups / Lot Tracking

- Scope Exclusion with a Click: Instantly filter out non-applicable assets like NFTs and wrapped tokens, ensuring focus on relevant crypto assets.

- Fair Value Calculation Across Classes: Accurately calculate changes in fair value for different asset classes, enhancing precision in financial reporting.

- Customized Lot Tracking: Tailor tracking and valuation of crypto assets across custom lots and wallet groupings, facilitating detailed and compliant fair value reporting.

One Data Set, Multiple Sets of Books

- Centralized Transaction Data: Easily manage diverse accounting treatments for the same transactions in one unified Bitwave system, eliminating the need for multiple instances.

- Multiple Sets of Books: With a click, access and tailor different sets of books, each with distinct valuation methods and settings, to align with specific accounting requirements.

- Compliant Fair Value Reporting: Enable accurate and compliant fair value reporting, especially for distinct tokens, with adaptable asset-by-asset valuation capabilities.

Flexible and Reliable Pricing

- Advanced Pricing Engine: Leverage reliable pricing data like CryptoCompare’s CCCAGG, a comprehensive pricing source that draws from an extensive exchange pool.

- Flexible Time Frame Pricing: Offers the flexibility to select pricing snapshots within a range from low/high/average hourly rates to specific time points, ensuring consistent application of valuation methods.

- Waterfall Pricing: Allows for a hierarchical application of pricing sources, ensuring that valuation remains accurate even when primary sources are unavailable.

Audit-Ready Reports

- Pricing Report: Illustrate the valuation process with pricing sources, methodologies, and timestamps, ensuring each asset is priced with accuracy and consistency.

- Actions Report: Map the journey of each asset lot, showing cost basis, gains, losses, impairments, acquisitions, and disposals.

Take the Next Step

Schedule a demo with Bitwave to explore how we can help you effortlessly navigate the new FASB crypto fair value rules.

Disclaimer: The information provided in this blog post is for general informational purposes only and should not be construed as tax, accounting, or financial advice. The content is not intended to address the specific needs of any individual or organization, and readers are encouraged to consult with a qualified tax, accounting, or financial professional before making any decisions based on the information provided. The author and the publisher of this blog post disclaim any liability, loss, or risk incurred as a consequence, directly or indirectly, of the use or application of any of the contents herein.