Get ready. Crypto tax season is about to get a whole lot more… official.

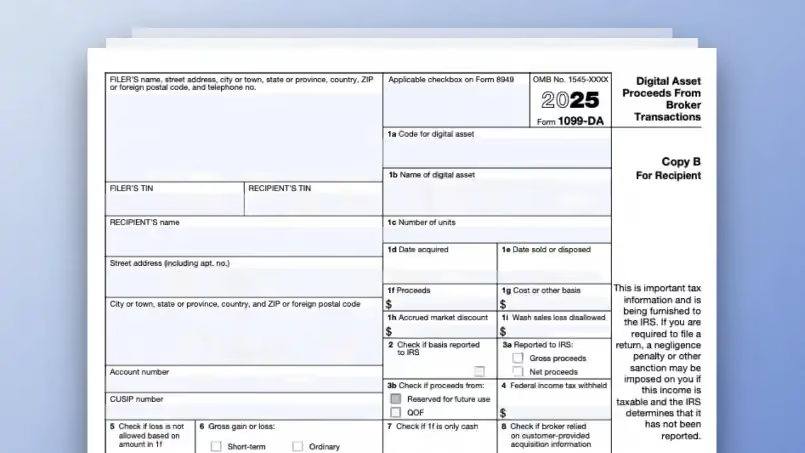

Starting in 2025, if you’ve traded, sold, or swapped digital assets through a broker, you can expect a Form 1099-DA to land in your (and the IRS’) inbox.

This new tax form isn’t just another piece of paperwork, though. It’s the government’s way of making sure crypto transactions get the same level of scrutiny as stocks and other non-crypto financial instruments.

For businesses and investors, that means it’s time to get your crypto accounting in order.

Knowing what’s on 1099-DA, how it affects your tax filings, and how to avoid tax season headache is key. We’re breaking it all down so you can stay ahead of the curve.

Who Receives a 1099-DA?

If you’ve traded or sold digital assets through a broker (like Coinbase, Kraken, or Gemini), you’ll likely receive Form 1099-DA. These platforms must report your gross proceeds, transaction details, and cost basis (if available) to both you and the IRS.

However, if you’re only holding digital assets with a non-custodial wallet or transacting on a truly decentralized platform, you may not receive a 1099-DA.

But, wait! That doesn’t mean you get a pass on taxes...

It just means the reporting obligation is completely on you, and not the exchange.

For businesses, this means ensuring that internal accounting systems accurately track transactions, even if a 1099-DA isn’t provided.

What’s on Form 1099-DA?

Based on the latest IRS guidance, Form 1099-DA includes:

- Personal Information: Name, address, and taxpayer identification number (TIN).

- Gross Proceeds: The total amount received from selling digital assets (not net profit, but the full sale price).

- Date of Sale: Exact timestamps for transactions.

- Type of Digital Asset: Whether it was Bitcoin, Ethereum, or another crypto asset.

- Units Sold: The number of tokens or coins moved.

- Cost Basis: The original purchase price of the sold assets (Important: Some brokers may not have this information or the technical capability to track it.)

- Holding Period: Whether the gain or loss is short-term or long-term.

- Transaction Type: Whether the digital asset was sold for cash, exchanged for another asset, or used for purchases.

- Fair Market Value (FMV): The price at the time of a transaction, particularly for swaps or purchases.

- Transaction Fees: Costs associated with executing the trade.

These individual elements are key to ensuring crypto tax compliance.

How Is 1099-DA Different from Other 1099 Forms?

If this sounds like a crypto version of 1099-B (used for stocks and securities), you’re not far off. But of course, with digital assets introduce added complexity:

- Price volatility affects cost basis tracking and tax calculations.

- Use cases beyond investing (e.g., payments, DeFi lending, staking) create unique tax implications.

- Blockchain-specific events (like forks, airdrops, and wrapped tokens) need special handling.

- Cross-border and decentralized transactions raise jurisdictional and reporting challenges.

Form 1099-DA is the IRS’s effort to close reporting gaps and enforce compliance.

When Does 1099-DA Reporting Begin?

Brokers are required to start issuing 1099-DA forms in early 2026 for the 2025 tax year.

The IRS has also provided transitional relief, so reporting may be incomplete in the first year as platforms adjust.

For businesses and investors, this means 2025 is the last tax year before full reporting kicks in. This means, now is the perfect time to ensure records are accurate and compliant – before the IRS starts receiving direct reports from brokers.

Special Rules for Stablecoins and NFTs

The IRS has introduced tailored reporting rules for two major asset classes: qualifying stablecoins and NFTs.

Stablecoins

Transactions with "qualifying stablecoins" (those pegged to a fiat currency, like USDC or USDT) are subject to a $10,000 annual de minimis threshold. If your total stablecoin transactions stay below this amount, brokers won’t report them.

For amounts above $10,000, brokers report aggregate totals rather than listing every individual transaction. This prevents excessive reporting on small, everyday transactions while still capturing major activity.

NFTs

NFTs have a different reporting threshold. If total NFT sales exceed $600 for the year, brokers must report them—but they can do so in aggregate rather than detailing every transaction.

Additionally, NFT sales are categorized as either primary (first sale by the creator) or secondary (resale in the market), as the IRS recognizes that these have different tax implications.

What About Privacy?

While crypto’s appeal often includes privacy and decentralization, tax compliance is a different matter.

The IRS isn’t requesting wallet addresses, private keys, or seed phrases, but it does expect accurate reporting of gains, losses, and taxable events.

For those who prioritize privacy, the best strategy is proactive record-keeping to ensure filings are accurate and align with reported data.

How Bitwave Simplifies Crypto Tax Reporting

With Form 1099-DA becoming a reality, businesses and investors need reliable systems to ensure compliance without added headaches.

Having an enterprise-grade crypto accounting system, like Bitwave, is essential.

- Automated transaction tracking from exchanges, wallets, and DeFi platforms.

- Real-time cost basis and gain/loss calculations for accurate tax reporting.

- 1099-DA reconciliation to ensure broker-reported data aligns with internal records.

- Multi-asset support, covering everything from Bitcoin and Ethereum to stablecoins and NFTs.

- Direct integration with leading ERP’s, reducing manual work.

Stay ahead of crypto tax compliance. Schedule a Bitwave demo today.

Final Thoughts

1099-DA reporting marks a major shift in how digital assets are taxed.

While 2025 is a transitional year, businesses and retail investors should use this time to refine their record-keeping processes and ensure tax filings align with IRS expectations.

By leveraging automation and expert tax solutions like Bitwave, you can stay compliant while focusing on what matters most – growing your business and investments

.

---760x420.avif)

Want to hear what the experts say about 1099-DA, along with other regulations like CARF and DAC8?

Spin over to Bitwave University for our on-demand webinar with S&P!

And the best part? You can earn one hour of NASBA-licensed CPE while you learn.

See you on BitwaveU!

Disclaimer: The information provided in this blog post is for general informational purposes only and should not be construed as tax, accounting, or financial advice. The content is not intended to address the specific needs of any individual or organization, and readers are encouraged to consult with a qualified tax, accounting, or financial professional before making any decisions based on the information provided. The author and the publisher of this blog post disclaim any liability, loss, or risk incurred as a consequence, directly or indirectly, of the use or application of any of the contents herein.

.avif)