The powers that be – specifically, the government and big banks – are still waging their quiet war on crypto.

In this issue of the Triple Entry newsletter, we’ll cover:

- The Treasury Department’s insane power grab

- Why JPMorgan CEO Jamie Dimon “would shut down crypto”

- Fact-checking the ‘crypto funds terrorism’ myth

- The enemy of Elizabeth Warren’s enemy is her friend

Here we goooooo!

“Calc”-you-later, 🧮

Trevor

U.S. Treasury asks for Broadest Expansions of Powers since the Patriot Act

The Treasury Department is emerging as the “final boss” in financial oversight over crypto. This isn't just another power grab by an agency head like Gary Gensler; it's far more significant.

Treasury’s Pitch to Congress

Deputy Secretary of the Treasury Wally Adeyemo is leading the charge in aggressively lobbying Congress for expanded powers to combat illicit financial activities using cryptocurrencies. Their wishlist is so voracious that it might just make Santa blush.

Central to their proposal is the push for jurisdiction over non-U.S. stablecoin issuers, notably Tether. This move clearly signals the Treasury's ambition to significantly amplify its enforcement and sanctions powers within the crypto sector.

The sickening irony here is that the Treasury's entire rationale for this massive expansion of power is that terrorist groups – including Hamas – "use new virtual methods to move, store and obfuscate their funding streams. These methods often include the use of evasive cryptocurrency networks and services, including mixers" (according to Adeyemo).

Fact-Checking the ‘Crypto Funds Terrorism Myth’

It’s the same rationale the Wild Witch of Web3 (Elizabeth Warren) continues to stand on, even after the WSJ’s disgraceful article, claiming that more than $90 million in crypto went to terrorist groups, was proven false by Elliptic, to whom the claim was attributed.

The reality is that Hamas began soliciting Bitcoin donations in 2019, realized these transactions were traceable on a public blockchain, then suspended crypto fundraising activity, citing “concern about the safety of donors and to spare them any harm.”

So, what’s the Treasury Department actually referring to?

The $21,000 in crypto donated since the October 7th Hamas attacks (that’s now been frozen)?

These are some high table stakes, folks.

The Treasury’s Outrageous Wishlist

We’ll give most of the credit to Austin Campbell, Founder and Managing Partner of Zero Knowledge Consulting, for this summary of what the Treasury is asking the Senate Banking Committee for. His analysis on X was impeccable.

Here’s what the Treasury is asking Congress for:

1. Designating Wallet Providers, Validator Nodes, and DeFi Services as Financial Institutions

"Define a new cryptocurrency-related category of “financial institution” under the BSA, which includes but is not limited to cryptocurrency exchanges, Virtual Asset Service Providers (VASPs), virtual asset wallet providers, certain blockchain validator nodes, and decentralized finance services and subject it to the type of AML/CFT requirements to which banks and other financial institutions are already subject."

Why it’s insane:

The Treasury's proposal is sweeping in scope. It aims to redefine “financial institutions” under the Bank Secrecy Act (BSA) to include a broad array of crypto-related entities. This expansion targets not just cryptocurrency exchanges and Virtual Asset Service Providers (VASPs) but extends to virtual asset wallet providers, some blockchain validator nodes, and DeFi services.

The implications of this proposal are significant:

- Security Risks and Practical Concerns: Requiring validator nodes and DeFi protocols to manage sensitive personal and financial data could lead to a highly insecure ecosystem. It's akin to asking a retailer like Amazon to conduct KYC on all its customers and store this sensitive data on systems vulnerable to cyber-attacks. It's critical to recognize that these entities are not financial institutions in the traditional sense.

- Overreach into Software and Infrastructure: The expectation for software providers (such as virtual wallet providers) and infrastructure components (like blockchain nodes) to conduct KYC is unprecedented. To use Campbell’s words, “This would be the equivalent of requiring KYC to use your web browser to get on the internet because you might transact, and requiring roads to KYC cars before they can pass down them because you might drive somewhere and buy something.” This approach overlooks the nature of software providers and infrastructure components as non-financial actors.

- A Narrower Focus Would Be Preferable: It would be more reasonable if the Treasury’s proposal were confined to exchanges and stablecoin issuers. These entities resemble traditional financial service providers in their control and knowledge of the platform and its transactions.

2. Unlimited Power Over All Elements of Cryptocurrency Transactions

"Create an explicit IEEPA (International Emergency Economic Powers Act) authority to designate blockchain nodes or other elements of cryptocurrency transactions."

Why it’s insane:

This part of the proposal, seemingly a response to concerns about platforms like Tornado Cash, is alarmingly broad. While there's an argument for designating specific protocols linked to criminal activities, the phrase “other elements of cryptocurrency transactions” is excessively vague. Such sweeping authority could lead the Treasury to arbitrarily designate almost any component associated with a blockchain transaction as suspect. This approach lacks the necessary precision and fairness expected in the application of sanctions.

3. Jurisdiction Over USD-Backed Stablecoins at Home and Abroad

"Clarify OFAC jurisdiction over USD-backed stablecoins," meaning, "Legislation could explicitly authorize OFAC to exercise extraterritorial jurisdiction over transactions in stablecoins pegged to the USD (or other dollar-denominated transactions) as they generally would over USD transactions."

Why it’s insane:

Asserting jurisdiction over USD-backed stablecoins, even those based and operating entirely outside the U.S., is a bold geopolitical move. This policy would signify the U.S. claiming authority over financial instruments domiciled in foreign nations, merely because they are pegged to the dollar.

The implications of such a policy could be far-reaching and potentially incendiary. It raises questions about the selective application of this authority and the risk of accelerating a global shift away from reliance on the U.S. dollar, particularly in the stablecoin space. The proposal seems to overlook the broader implications of such a unilateral assertion of financial control on the global stage.

The Triple Entry Take

Again, Austin Campbell hit the nail on the head here, so we’ll just insert his takeaway because it perfectly reflects how we feel:

“Overall, my read is this: there are some good basic points in here that I can get behind, but in general, Treasury is asking for the broadest expansions of powers since the Patriot Act, and in a way that makes a mockery of some of the technical details of modern communication with the side benefit of probably causing major geopolitical conflict due to the overreach. This is not a well-reasoned, balanced proposal. If they solely asked for sanctions authority for blockchain addresses / protocols to be clear, for KYC/AML to be required for exchanges and stablecoin issuers, and for some targeted sanctions tools, I'd be fine with this. But here, the ask is so insanely and profoundly over-broad, we'd be creating both a more overreaching and way jankier surveillance state than even China, which is very much not something the United States should be in the business of promoting. Doing something like the narrow approach is better than doing nothing, but doing nothing is way better than doing everything the Treasury asked for.”

How the Grinch Would Like to "Close Down Crypto" for Christmas

In today’s second story, we return once again to discussions happening at the seat of government in Washington DC, where powerful people who don’t know how to reset their own WiFi router are having opinions about technologies they don’t understand.

Last Wednesday, Dec. 6th, JP Morgan CEO Jamie Dimon graced the world with humbly-stated opinions on crypto during a routine hearing on regulating Wall Street before the Senate Banking Committee.

We are hard-pressed to find a better example of these remarks than this succinct statement from Mr. Dimon.

“If I was the government, I’d close [crypto] down.”

To which we say - we are glad you, sir, are not “the government.”

Look, we know JP Morgan is the largest U.S. bank by assets, but even so, the level of hubris it takes for one man - even if he is the CEO of JP Morgan - to sit before the Senate and say something like that is honestly pretty impressive. Unfortunately, it’s not as badass as a lone marshal in a lawless town of the Wild West saying, “I am the law around here,” but maybe Dimon always wanted to be Wyatt Earp.

Dimon hasn’t been shy about his (supposed) disdain for crypto - he’s been a vocal opponent of the industry since as early as 2014, calling it a “hyped up fraud” and a “pet rock,” among other things. His primary objection, however, is that crypto exists primarily as a smokescreen behind which bad actors can hide, and he has been surprisingly consistent on this stance for nearly a decade.

“The only true use case for [crypto] is criminals, drug traffickers … money laundering, tax avoidance,” he said during the hearing.

Good thing there were no banks involved in some of the biggest money laundering scandals of the past fifty years.

We’ve got some thoughts on all this, including the suspicion that “the lady doth protest too much.”

Criminals, Drug Traffickers, AND Tax Avoiders? In this economy?

First, an acknowledgment: the unfortunate link between crypto and criminals is there (see last Entry's coverage of CZ, Binance, charges being pled guilty to, etc. etc.), but the argument that it is the industry's primary use case and function is simply untrue.

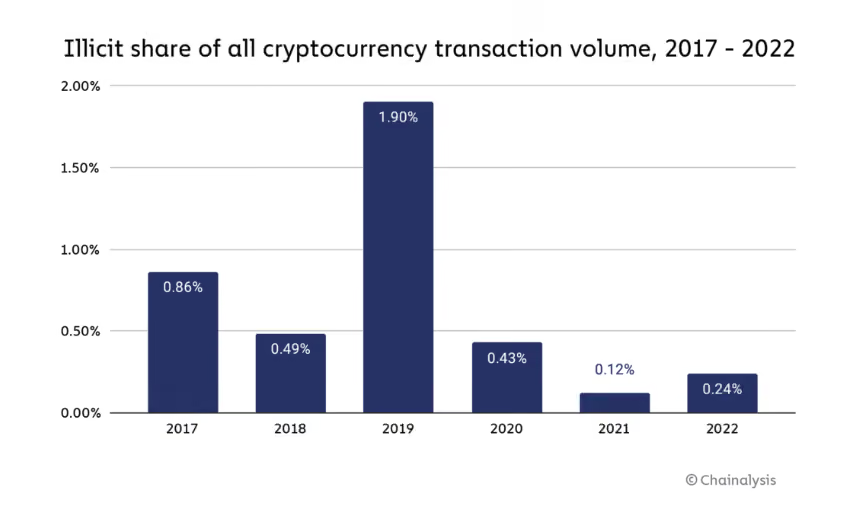

In their 2023 crypto crime trends report published earlier this year, Chainalysis pointed out that although 2022 saw an increase in the share of all cryptocurrency activity associated with illicit activity - for the first time since 2019 - the actual percentages of those numbers relative to all cryptocurrency transaction volume were 0.12% in 2021 and 0.24% in 2022.

Just to restate this - the estimated percentage of crypto activity that could be considered illegal or “illicit” is…less than 1%. With those numbers, if you’re trying to make the case that the Al Capones and Pablo Escobars of the world are the primary users of crypto, there’s an awful lot of transaction volume going unaccounted for (pun intended) in your analysis.

So, what else might be going on with Dimon’s unflagging adherence to this narrative?

TradFi Wants to Run Unopposed

In a way we feel like this is just characters playing the roles they’ve been written.

Crypto, by nature, exists as an antithesis to TradFi’s entire way of life, and institutions like JP Morgan are not really advantaged by the crypto industry becoming a legitimate competitor - dare we say threat? - to that way of life. So, at first blush, it makes sense that Dimon would want to see crypto gone, the same way anybody interested in winning in the marketplace would like to see fewer competitors.

But it goes further than that. It’s worth noting that despite these public comments denouncing the crypto industry, JP Morgan is one of several giants of legacy finance investing in blockchain tech; just last month JPM announced a partnership with Apollo Global and Avalanche toward creating a blockchain-based asset management proof-of-concept, a subproject of the Monetary Authority of Singapore’s Project Guardian.

Also worth noting: back in 2018, the bank filed a US patent application for a distributed ledger technology payments system. (Note: for some reason the link to the actual filing is broken but there are still press records of it being filed, so we felt comfortable including this info in this story).

So basically, all we’re hearing is “We’d like to see crypto gone so we can have an unimpeded path to build a centralized version of what crypto is doing.”

The Enemy of Elizabeth Warren’s Enemy is Her Friend

Last Wednesday’s hearing featured a guest appearance by none other than our very own “wicked witch of web3,” Elizabeth Warren, who delivered most of the questions to Dimon throughout the hearing (read: both parties gave each other a layup). Warren - typically an antagonist for the banking industry just as much as she is for the crypto industry - decided to just be a crypto antagonist for the day, as she echoed Dimon’s sentiments of cryptocurrency fueling illicit activity.

"When it comes to banking policy, I am not usually holding hands with the CEOs of multi-billion dollar banks, but this is a matter of national security," she said. Yes, of course it is, Elizabeth, and how convenient that you’ve found a new ally in your well-documented fight against the crypto industry. As the saying goes, “The enemy of my enemy is my friend.”

And how convenient that all eight big bank CEOs present at the hearing agreed with Warren’s position that the crypto industry should be subject to the same anti-money laundering functions as centralized financial institutions.

And how convenient, finally, that just this past Monday Warren gained five new Senators in support of her proposed Digital Asset Anti-Money Laundering Act, which would - we remind you - effectively outlaw crypto in the US by requiring the sort of compliance functions that - by design - cannot be performed by non-custodial, decentralized technologies.

We have written about this bill in this newsletter before, and it’s a doozy to read through the thing and see how it’s not only anti-crypto, it’s flat-out anti-privacy and anti-autonomy, making illegal a whole host of items involved in decentralized finance down to the level of validators and DeFi front ends.

The Triple Entry Take

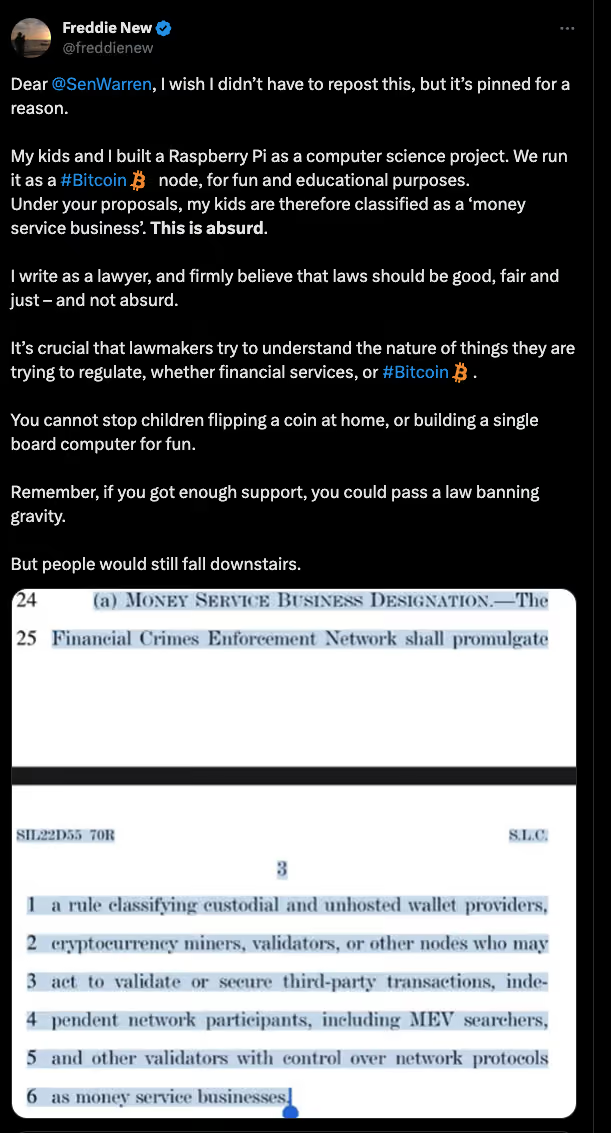

Last week’s hearing feels like political back-scratching more than anything - two groups deciding to play nice and say the right lines to each other to build support for their common cause of crippling or full-on eliminating crypto from the playing field. But frankly, even if Warren’s bill passes, we wonder if all it will really do is drive the innovations of crypto underground, out of sight. We’ll let this Tweet from Freddie New close out this story.

Spotlight 🔦 - We Wrote the Guide on Audit-Readiness

Imagine playing chess, but with a few extra pieces thrown in that can move in completely unconventional ways.

That's what digital asset audits are like: they take the familiar rules of traditional auditing and add new dimensions of complexity.

Rapid technology evolution, regulatory ambiguities, and the intricacies of blockchain are all part of the puzzle with digital asset audits, in a way that just doesn’t exist within traditional audit frameworks.

Most companies find digital asset audits perplexing because they have trouble applying those traditional audit frameworks to new blockchain-enabled business environments.

While the foundational principles of auditing remain the same—assessing compliance, verifying assets, and ensuring accurate financial reporting—the incorporation of digital assets introduces layers of complexity.

Want to learn how to navigate those layers of complexity? Our brand new email course, The Digital Asset Audit Survival Guide, is NOW LIVE!

The best part? It's still free.

The Water Cooler 🚰

Things worth talking about at the office water cooler…if you 1) talk to people, 2) still work in an office, and 3) have a water cooler.

Other Significant Findings

The IRS wants its cut from FTX before anyone else.

Extraordinary Items 🤓

Is this allowed? We don’t know, but we’re doing it anyway.

Disclaimer: The information provided in this blog post is for general informational purposes only and should not be construed as tax, accounting, or financial advice. The content is not intended to address the specific needs of any individual or organization, and readers are encouraged to consult with a qualified tax, accounting, or financial professional before making any decisions based on the information provided. The author and the publisher of this blog post disclaim any liability, loss, or risk incurred as a consequence, directly or indirectly, of the use or application of any of the contents herein.