Happy new year, everybody! Things are happening. And boy, are they happening.

6050I: But, WHY? The new $10K+ Crypto Reporting Rule Explained

Sure, the Bitcoin ETFs are exciting, but let’s be honest:

The news you’re most focused on this week is the new $10K+ crypto transaction reporting rule, otherwise known as 6050I. So let's get into it.

Last week, Jerry Brito, Executive Director posted on X about the new law. In short time, Crypto Twitter looked like this:

What does 6050I require?

As of January 1, 2024, if you receive $10k or more in crypto, you now must report the transaction (including names, addresses, SSN/ITIN numbers, amount paid, date, nature of transaction, etc.) to the IRS within 15 days under threat of a felony charge.

The rule actually isn’t new; it’s an anti-money-laundering bill that’s been around since 1984, but the Infrastructure Bill signed into law by President Biden updated 6050I to include digital assets.

Traditionally, under Section 6050I of the Internal Revenue Code (IRC), any individual involved in a trade or business who gets over $10,000 in cash from a single transaction (or a series of related transactions) is mandated to declare this on Form 8300.

Who 6050I applies to

The law primarily applies to those who receive crypto receipts of more than $10k IN THE COURSE OF A TRADE OR BUSINESS (there’s a reason that’s in all caps – lots of confusion here).

Where it gets interesting is the term "trade or business" is broadly defined and subject to interpretation. The courts and IRS often look at several factors to determine if any activity qualifies as a trade or business, including:

- Regularity and continuity of the activity

- Intent to make a profit

- Level of activity

Retail traders typically aren't seen as a "trade or business," but things could get tricky if you trade frequently, run validator nodes, engage in staking, etc.

Is 6050I actually in effect?

First, a disclaimer: we aren’t attorneys nor legal experts, so this most certainly is not legal advice.

But we can tell you what attorneys and legal experts have said on the matter.

For reference, most of our information comes from this X exchange between Jerry Brito and CryptoTaxGuy.ETH.

The big question here is whether or not 6050I is “self-effectuating” – that the the law automatically comes into effect without the need for additional regulations or guidance.

CryptoTaxGuy.ETH's Take:

- He acknowledges the unusual stance of the DOJ/IRS, suggesting the 6050I section isn't self-executing for crypto without specific regulations.

- He points out that while there are existing regulations for cash payments, the inclusion of digital assets in the 6050I(d)(3) section from January 1, 2024, should, in theory, make the rule self-executing.

- However, based on statements from the DOJ and IRS, there seems to be a temporary reprieve. CryptoTaxGuy.ETH pragmatically advises not to challenge this stance, as it may offer a defense against potential penalties for "intentional disregard."

Jerry Brito's Perspective:

- Brito concurs with the practical approach but differentiates between practical and legal realities. He emphasizes that DOJ arguments and unofficial IRS statements are not legally binding.

- He criticizes this approach as counterintuitive to the rule of law, arguing that the public can't be expected to follow non-binding, informal communications over the actual text of the law.

- Brito suggests that while the IRS lacks the authority to nullify the law, they could potentially delay enforcement until a clear compliance mechanism is established.

Where guidance is needed

As you can imagine, 6050I leaves us with a lot of unanswered questions.

If you know anyone over at the IRS, please let them know that they have an entire industry looking for answers.

Here’s a non-comprehensive list of areas needing clarification (shout-out to EisnerAmper for putting these together):

- When will a transaction with a digital asset be considered a trade or business transaction versus an investment?

- What form will be filed – Form 8300 or a new form?

- How will the recipient of a digital asset file the form when they do not know the sender and have no way to obtain the required information?

- How will receipt of digital assets in situations such as airdrops or hard forks be treated if the FMV exceeds $10,000?

- How will mining and staking rewards be treated?

- How will “related” transactions be determined with digital assets?

- How will the form be filed for taxpayers involved in decentralized exchange transactions?

So, What's Next?

Given these perspectives, it's apparent that the application of 6050I to crypto is still in a state of flux. Despite the law's text, the practical approach, for now, seems to be a watchful waiting. But, then again, you’d technically be breaking the law, so it’s probably best to comply the best you can.

Keep an eye out for any official statements from the IRS clarifying their stance. We will, of course, keep our ear to the ground and keep you updated!

_______

Spot BTC ETF? LFG!

If the Spot Bitcoin ETF saga was a rom-com, it'd be the spitting image of 'Just Friends' with Ryan Reynolds.

Picture this: Chris Brander, our Bitcoin hero, starts off as the dorky high school kid (you know, Bitcoin in its early days) totally smitten with Jamie Palamino - the SEC.

Fast forward ten years, and voilà, Chris is now this suave, successful guy, just like Bitcoin hitting the big leagues. But Jamie keeps playing hard to get, always friend-zoning Chris at every turn. It's the classic 'will they, won't they' with a side of financial drama – Bitcoin leaning in for a smooch of approval, and the SEC turning its cheek, again and again.

Well, folks, we’re finally getting to the end of the movie and sparks are about to fly.

What’s the Status?

There’s basically a 99% likelihood that the Spot Bitcoin ETFs get approved at this point.

The SEC’s approval deadline is on Wednesday (Jan. 10th) and CNBC reported that it expects the ETFs to be approved Wednesday and possibly begin trading this week.

The SEC issued additional comments on pending applicants’ S-1 forms Monday night, which some called a “delay signal.” Others took it as a good sign that the SEC turned comments around so quickly – something they certainly wouldn’t do if they were going to deny the applications.

The Fee War

On Monday, ETF applicants hurriedly updated their S-1 filings as an all-out fee war broke out:

- BlackRock: dropped its fees from 0.3% to 0.2% for the first 12 months, or until $5B volume is hit

- Ark Invest: lowered its fees from 0.8% to 0.25%, NO FEES for the first 6 months or until $1B in volume

- Galaxy: 0.59% fee, fees waived for the first 6 months or until $5B volume.

- Grayscale: dropped its fees from 2% to 1.5%.

- WisdomTree: 0.5%

- VanEck: 0.25%

- Valkyrie: 0.8%

- Fidelity: 0.39%

These fees are much lower than expected.

To put things in context, it costs less to hold a Bitcoin ETF for a year than a single trade on Coinbase. (~40-60bps vs ~25bps for a retail size trade).

But, why such low fees?

Because they’re all banking on billions flowing into the ETFs the moment they’re approved. They all want to be your first choice.

Where does Bitcoin go from here?

No one knows. Some say it’s a “buy the rumor, sell the news” event and others say it’s a “buy the rumor, buy the news” event. We’re not big speculators, so here’s a “curation of speculation” for you:

- Standard Chartered: $50 - 100B of spot Bitcoin ETF inflows in 2024 and a price of $200,000 by the end of 2025.

- Messari: “We probably won’t see another 100x for Bitcoin, but the asset could easily outperform other established asset classes once again in 2024. Eventual parity with gold would yield a price per BTC of over $600,000.”

- VanEck: New all-time-high in 2024 led by Bitcoin inflows that mimic gold post-ETF

- Bitwise: Above $80,000

- Google Bard: $120,000

- My Grandma: “What’s Bitcoin?”

And perhaps the most important (and reliable) indicator of them all: Inverse Cramer.

Jim Cramer says "Bitcoin is topping out,” so sell the house and buy more Bitcoin (jk, don’t actually do that).

One final note: VanEck's Matthew Sigel said he heard from a well-placed source that BlackRock has $2 billion of capital lined up from existing bitcoin holders who want to rotate into spot bitcoin ETFs in week one.

Things could get crazy.

_______

The Water Cooler 🚰

Things worth talking about at the office water cooler…if you 1) talk to people, 2) still work in an office, and 3) have a water cooler.

Other Significant Findings - Our 2023 Recap

A year ago the Triple Entry team marched boldly into the new year with five predictions for crypto (and for ourselves!) in 2023. A lot has changed since then, and since we’ve already done a fair bit of guessing (dare we say, predicting) for 2024 in this newsletter, we thought we’d do one last tour through the year that recently was and see whether or not we have the gift of prophecy.

The Triple Entry Crypto Crystal Ball 2023

🔮 Our 2023 Market Prediction 🔮 - Ethereum flips Bitcoin in market cap.

Accuracy: Swing and a miss

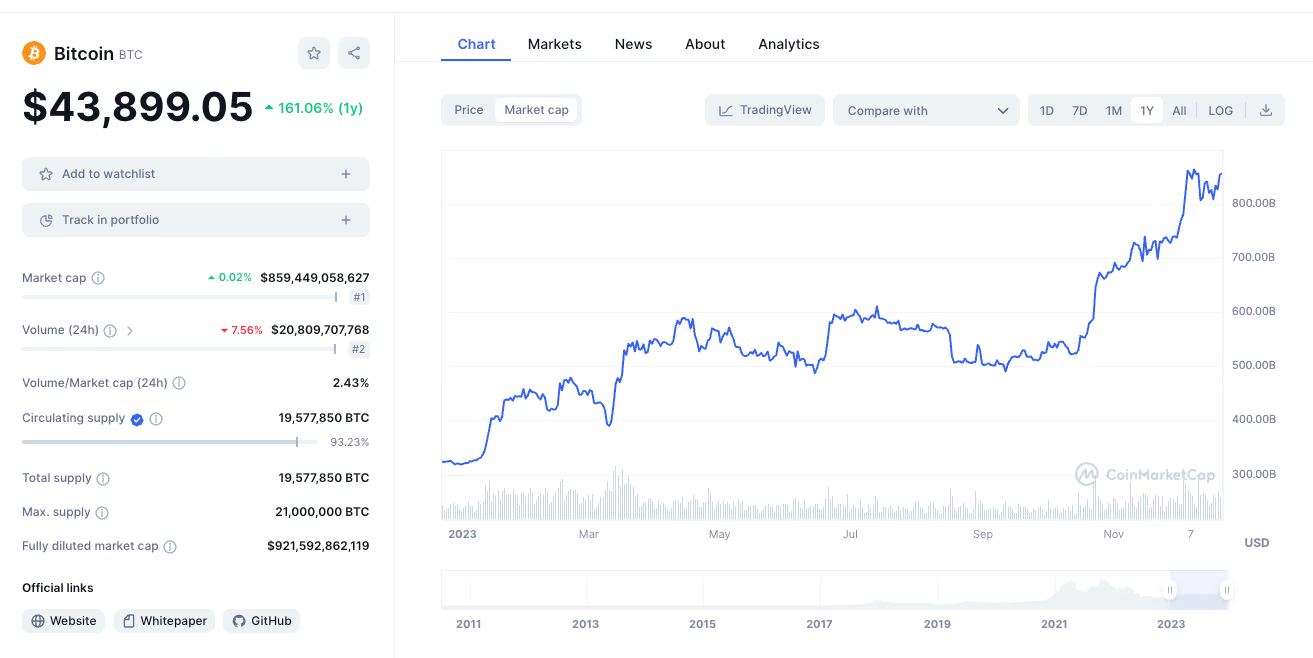

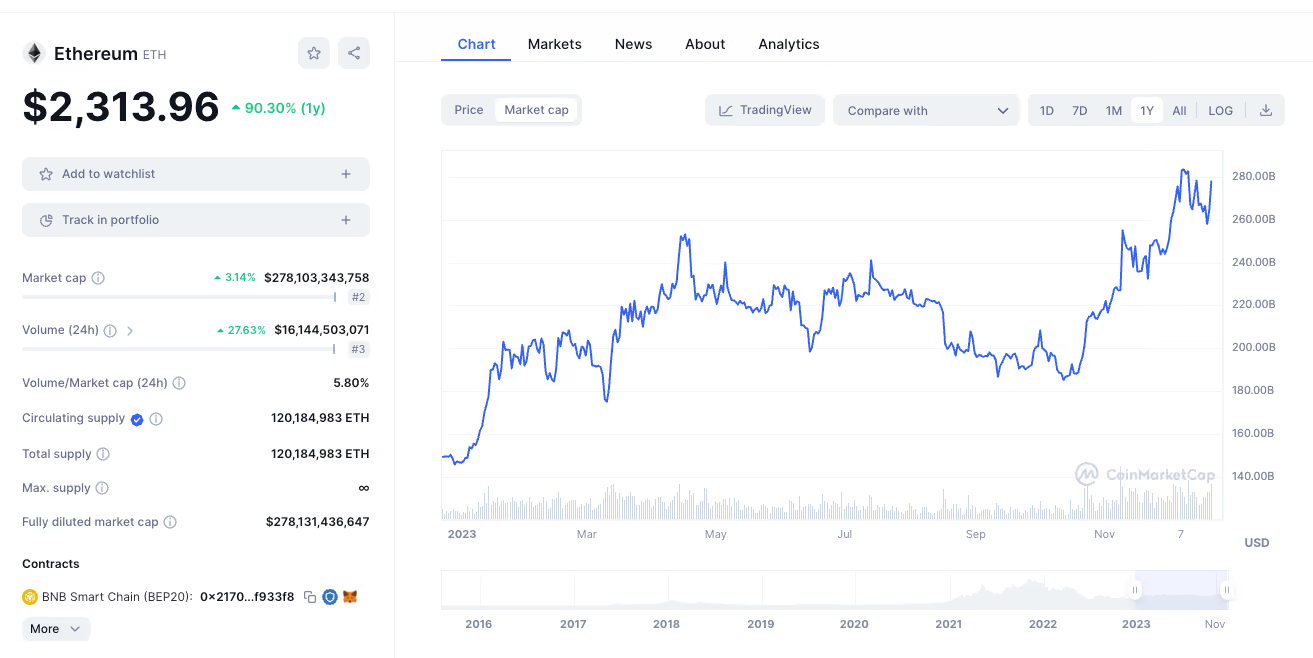

Unfortunately, we didn’t stick the landing on this one. Ethereum saw some nice growth in 2023 after The Merge successfully transitioned from a Proof-of-Work to Proof-of-Stake consensus mechanism. things like staking (and re-staking!) gained greater traction but as we’ve already covered here - the OG cryptocurrency is still king - whether you believe it’s actually going to $1 million or not. Bitcoin and Ethereum closed out 2023 with a market cap of $855.01B and $278.35B, respectively.

Bitcoin Market Cap

Jan. 1 2023 - $318.07B

Dec. 22 2023 - $855.01B

Ethereum Market Cap

Jan 1 2023 - $146.98B

Dec. 22 2023 - $278.35B

🔮 Our 2023 Accounting Prediction 🔮 - We’ll get serious about crypto audits.

Accuracy - Nailed it (more or less) 🎯

This prediction wasn’t necessarily about actual crypto audits (although those were and are still prominent thoughts on our minds so much that we wrote the guide on how to prepare for one). More than anything, it was a prediction that after the events of FTX, the crypto industry would wake up to the need for accountants in order to achieve any kind of traction as a legitimate financial system. Last year certainly saw plenty of events in crypto that required accounting’s finest to rise to the challenge - from the Silicon Valley Bank meltdown to the slow motion train wreck of Binance.

🔮 Our 2023 Tax Prediction 🔮 - The IRS will crack down on tax compliance.

Accuracy - Nailed it 🎯

Remember when we all sat up and took notice of the whole “87,000 new IRS agents in training” thing, and how the 2022 infrastructure bill claimed that better tax collections from crypto investors would yield a $28 billion increase in receipts or 5% of the total bill’s expenditures? We headed into 2023 with every reason to believe that the IRS would stop playing nice (like they usually do, of course) and come for its pound of flesh hiding in crypto. And it wasn’t all about tax compliance either. Between their musical chairs of John Doe summonses against Kraken, Coinbase, and Circle, the shiny new Form 1099-DA with its host of cost basis concerns, the headache-inducing guidance on how staking rewards are taxed, and the proposed regulation that defines when someone involved in cryptocurrency qualifies as a "broker" under tax law, the IRS had it out for crypto in 2023.

🔮 Our 2023 Policy Prediction 🔮 - Gary Gensler and Elizabeth Warren will duke it out for the title “Most Hated Person in Crypto.”

Accuracy - Nailed it 🎯

It’s not like they tapped gloves and squared off to win the golden belt saying “Crypto Hates Me Most,” but you’d have thought these two really did agree to make it a competition. Gary Gensler and the SEC were out there suing everybody - Coinbase, Binance, and probably the local mom and pop pizza shop for good measure. Meanwhile, Elizabeth Warren, aka “the wicked witch of web3,” worked tirelessly to build an anti-crypto army; by the end of the year, she had gained bipartisan support for her proposed Digital Asset Anti-Money Laundering Act and got the CEO of the largest U.S. bank on her side regarding the (overstated) concerns of crypto’s fueling of “illicit activity.” Honestly, between the two of them, we’re not sure we’re able to hold up one of the gloves and declare a KO.

🔮 Multisig Prediction 🔮 - We’ll issue 10,000 CPE certificates.

Accuracy - Not so much

This was more of a “dare to dream” prediction, and we would’ve been surprised if we were right about it anyway. If you’re new here, when we first started writing this newsletter, it was under the banner of a crypto CPE provider and news outlet called Multisig Media. Well, Multisig became a Bitwave company last year, and though we didn’t issue 10,000 CPE certificates, we did launch BitwaveU, your knowledge hub for a variety of CPE-certified crypto accounting courses that won’t just inform you, they'll transform you. We’ve got big plans for the content we’ll be adding to BitwaveU in 2024, and we hope you’ll stick with us to see what happens!

Extraordinary Items

The memes have been fast and furious on crypto Twitter as we gear up for (hopefully) some exciting news about ETF approval. Here's one of our favs.

FAQs About $10k Crypto Reporting Rule (6050i), Explained

What does 6050I require?

As of January 1, 2024, if you receive $10k or more in crypto, you now must report the transaction (including names, addresses, SSN/ITIN numbers, amount paid, date, nature of transaction, etc. ) to the IRS within 15 days under threat of a felony charge.

Who 6050I applies to?

The law primarily applies to those who receive crypto receipts of more than $10k IN THE COURSE OF A TRADE OR BUSINESS (there’s a reason that’s in all caps – lots of confusion here). Where it gets interesting is the term "trade or business" is broadly defined and subject to interpretation.

Is 6050I actually in effect?

First, a disclaimer: we aren’t attorneys nor legal experts, so this most certainly is not legal advice. But we can tell you what attorneys and legal experts have said on the matter.

Where guidance is needed?

As you can imagine, 6050I leaves us with a lot of unanswered questions. If you know anyone over at the IRS, please let them know that they have an entire industry looking for answers.

So, What's Next?

Given these perspectives, it's apparent that the application of 6050I to crypto is still in a state of flux. Despite the law's text, the practical approach, for now, seems to be a watchful waiting.

Disclaimer: The information provided in this blog post is for general informational purposes only and should not be construed as tax, accounting, or financial advice. The content is not intended to address the specific needs of any individual or organization, and readers are encouraged to consult with a qualified tax, accounting, or financial professional before making any decisions based on the information provided. The author and the publisher of this blog post disclaim any liability, loss, or risk incurred as a consequence, directly or indirectly, of the use or application of any of the contents herein.