Do you have to pay taxes on crypto airdrops?

According to the IRS, airdrops are taxable events. Yep, that free bag of digital coins isn't so free after all. It's considered ordinary income, and it's taxed at your regular income tax rate.

Also, if you later sell what you received from the airdrop, you may also be subject to capital gains tax.

This FAQ covers all that and more, pulling back the curtain on the taxing reality behind crypto airdrops. Let’s reveal some truths.

How do I report receiving an airdrop on my taxes?

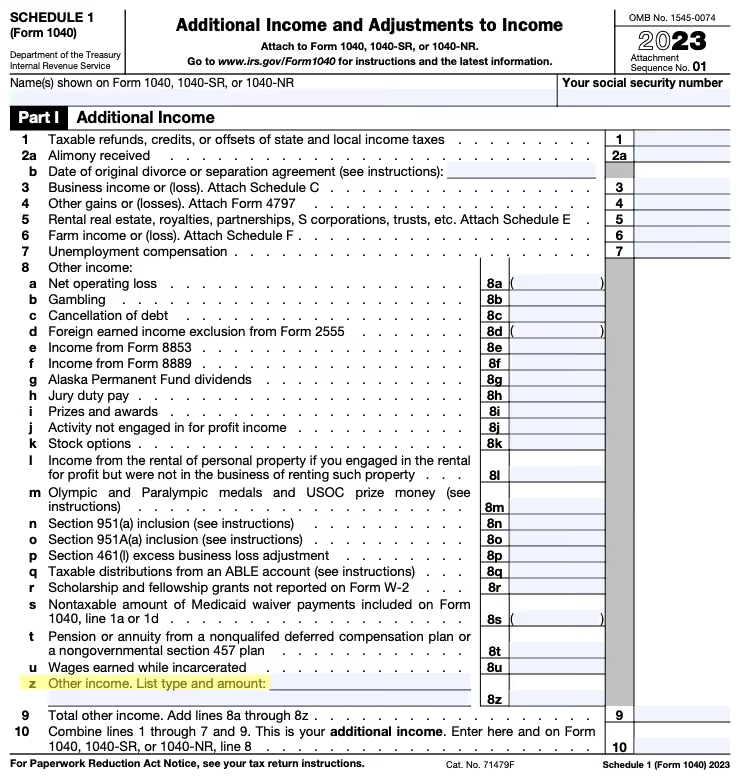

You would claim airdrops on your taxes using IRS Form 1040 Schedule 1. Specifically, the income from the airdrop would be reported as "Other income" on line 8.

The amount of income you report would be the fair market value of the crypto at the time you received the airdrop.

Generally, the fair market value is recorded on the distributed ledger at the date and time you received it, but it is possible to constructively receive crypto prior to the airdrop being recorded on the ledger. It’s also possible you do not have receipt of the crypto when the airdrop is recorded. For example, if your wallet is managed through a crypto exchange and the exchange doesn’t support the newly-created coin, the airdrop is not immediately credited to your account. In this case, the IRS considers you not to “exercise dominion and control” over the crypto. Only when the airdropped crypto becomes available in your wallet can you determine its fair market value.

How do I report selling crypto from an airdrop on my taxes?

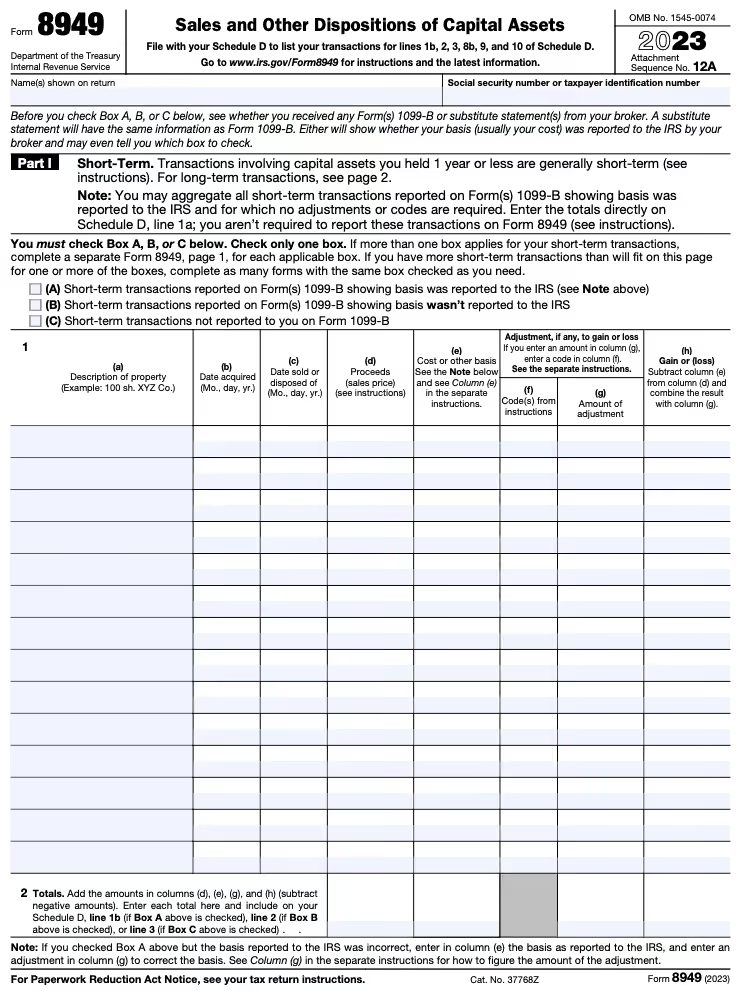

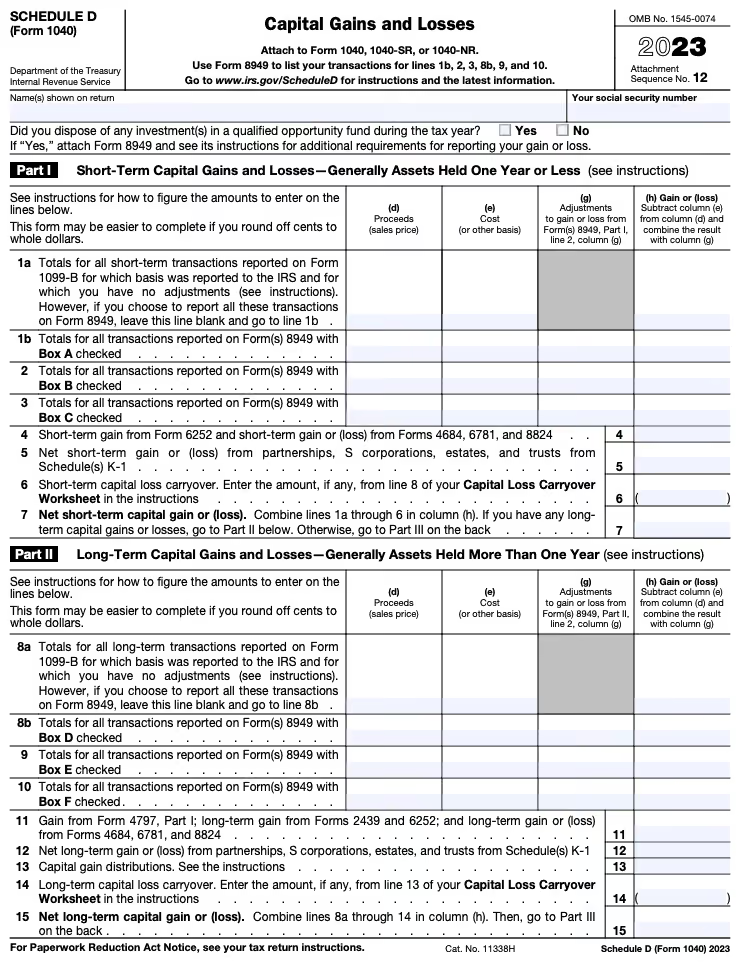

Selling, exchanging, or otherwise disposing of crypto you've received from an airdrop can result in a capital gain or loss. The IRS requires you to report these transactions on Form 8949 and Schedule D.

Form 8949 is where you'll detail each of your crypto transactions, including the date you received the airdrop, its fair market value (which becomes your cost basis), and any subsequent sale details.

Schedule D is your summary of capital gains and losses, where the information from Form 8949 will eventually land.

Capital gains are taxable, and the rate depends on how long you held the crypto before selling it. If you held it for more than a year, it's considered a long-term capital gain, which is usually taxed at a lower rate than ordinary income. If you held it for a year or less, it's a short-term capital gain, which is taxed at the same rate as ordinary income. Capital losses can be used to offset capital gains and reduce your tax liability.

How is the cost basis of an airdrop calculated?

The cost basis of an airdrop is the fair market value at the time you received it. Then the difference between the sale price and your cost basis is your capital gain or loss. If the sale price is higher than your cost basis, you have a capital gain. If it's lower, you have a capital loss.

Are free airdrops taxable?

Yes, they are. Even though you didn't ask for them, even though you didn't buy them, they're considered income because the airdropped crypto has a fair market value. It's like someone throwing a bag of money into your yard and then the IRS showing up saying you owe taxes on it. It's a strange world we live in, but that’s how it is.

How are NFT airdrops taxed?

NFT airdrops are taxed the same as other airdrops. The fair market value of the NFT at the time of receipt (or when a market becomes available) is considered taxable income. Report this as "Other income" on Form 1040 Schedule 1, line 8 as explained above.

If you later sell the airdropped NFT, you'll be subject to capital gains tax. The cost basis is the fair market value you reported as income when you received the airdrop.

Keep meticulous records of when you receive NFT airdrops and their fair market value at that time. This information is crucial for accurate tax reporting and calculating any future capital gains or losses.

Is an airdrop a gift?

In the traditional sense, you might think so. But in the eyes of the IRS, it's not.

Gifts are usually given out of "detached and disinterested generosity" (as the IRS puts it). Airdrops, however, are often intended to stimulate interest in a new coin, increase an exchange’s user base, or otherwise benefit the entity conducting the airdrop. There's no personal relationship between the giver and the receiver.

So, while it might feel like Christmas morning when you receive an airdrop, it's more like a paycheck in the eyes of the taxman.

Keep meticulous records

The IRS loves documentation, and in the fluctuating world of crypto, you'll want to have all the details at your fingertips.

That’s where crypto tax tracker Bitwave comes in. Bitwave is designed specifically to handle the unique challenges of enterprise crypto accounting. It can help you keep track of your airdrops, calculate their fair market value at the time of receipt, and even keep track of any subsequent sales or disposals. It provides a clear and organized record of all your transactions, making it easier to fill out those IRS forms correctly and confidently.

So, as we conclude our journey through the world of airdrops and taxes, consider giving Bitwave a try. It's not just software; it's your partner in navigating the ever-evolving landscape of DeFi taxation. Turn the complex into the comprehensible with Bitwave.

Disclaimer: The information provided in this blog post is for general informational purposes only and should not be construed as tax, accounting, or financial advice. The content is not intended to address the specific needs of any individual or organization, and readers are encouraged to consult with a qualified tax, accounting, or financial professional before making any decisions based on the information provided. The author and the publisher of this blog post disclaim any liability, loss, or risk incurred as a consequence, directly or indirectly, of the use or application of any of the contents herein.